Your home’s foundation is the bedrock of your family’s security and a cornerstone of your net worth. Yet, the insurance policy designed to protect it is often a blueprint for disappointment. Standard policies treat foundation damage not as a catastrophe to be solved, but as a maintenance issue to be excluded. This creates a critical vulnerability in your financial fortress, a gap that can compromise decades of asset growth. True asset protection demands a strategic approach that moves beyond default settings and constructs a defense built for certainty, not chance.

The Default Position: Deconstructing Standard Policy Exclusions

A standard homeowners policy, an HO-3 form, is the default blueprint for residential risk management. This blueprint contains specific, intentional exclusions for foundation damage that stem from gradual, predictable events. Understanding these built-in limitations is the first step in constructing a more resilient financial structure. Insurers view your home’s foundation through the lens of sudden, accidental events versus slow, inevitable decay. The policy is engineered to respond to the former, while explicitly walling off the latter.

Earth Movement and Settling: The Foundational Exclusions

Your policy almost universally excludes damage from “earth movement.” This broad category includes soil expansion and contraction, shifting, and subsidence. For homeowners in regions with expansive clay soils, like Texas, this exclusion is a significant structural risk. The insurer’s position is pragmatic: soil is inherently unstable and its movement is a natural, expected phenomenon. The gradual cracking and shifting that result from this movement fall under homeowner maintenance, not an insurable peril. The policy does not act as a warranty against geology.

Gradual Damage and Wear: The Inevitable vs. The Insurable

Insurance contracts are designed to cover sudden and unforeseen losses. They are not maintenance plans. Gradual damage, a slow-moving deterioration, is a core policy exclusion. This includes foundation issues arising from long-term water seepage, material fatigue, or deferred upkeep. For example, a hairline crack that expands over five years is a maintenance issue. An insurer categorizes this as predictable wear and tear, the operational cost of homeownership. This distinction is critical: the policy serves as a financial shield for unexpected accidents, not as a budget for age-related repairs.

Construction Defects and Faulty Workmanship

Your homeowners policy is not a backstop for poor construction. If your foundation fails due to substandard materials, improper concrete curing, or a failure to adhere to building codes, the liability rests with the builder, not your insurance carrier. These issues are classified as construction defects or faulty workmanship. Pursuing a remedy requires action against the responsible contractor. An insurance policy protects you from future, accidental events; it does not correct the errors of the past.

The Fortress Breach: Pinpointing Covered Perils for Foundation Damage

While standard exclusions create a formidable barrier, specific events can breach the fortress and trigger coverage. The key qualifier is always the source of the damage. Coverage activates when the foundation is damaged by a “covered peril,” a specific event named in your policy. The damage must be a direct result of this sudden and accidental incident, not a pre-existing condition exacerbated by it. This is the strategic entry point for a successful claim.

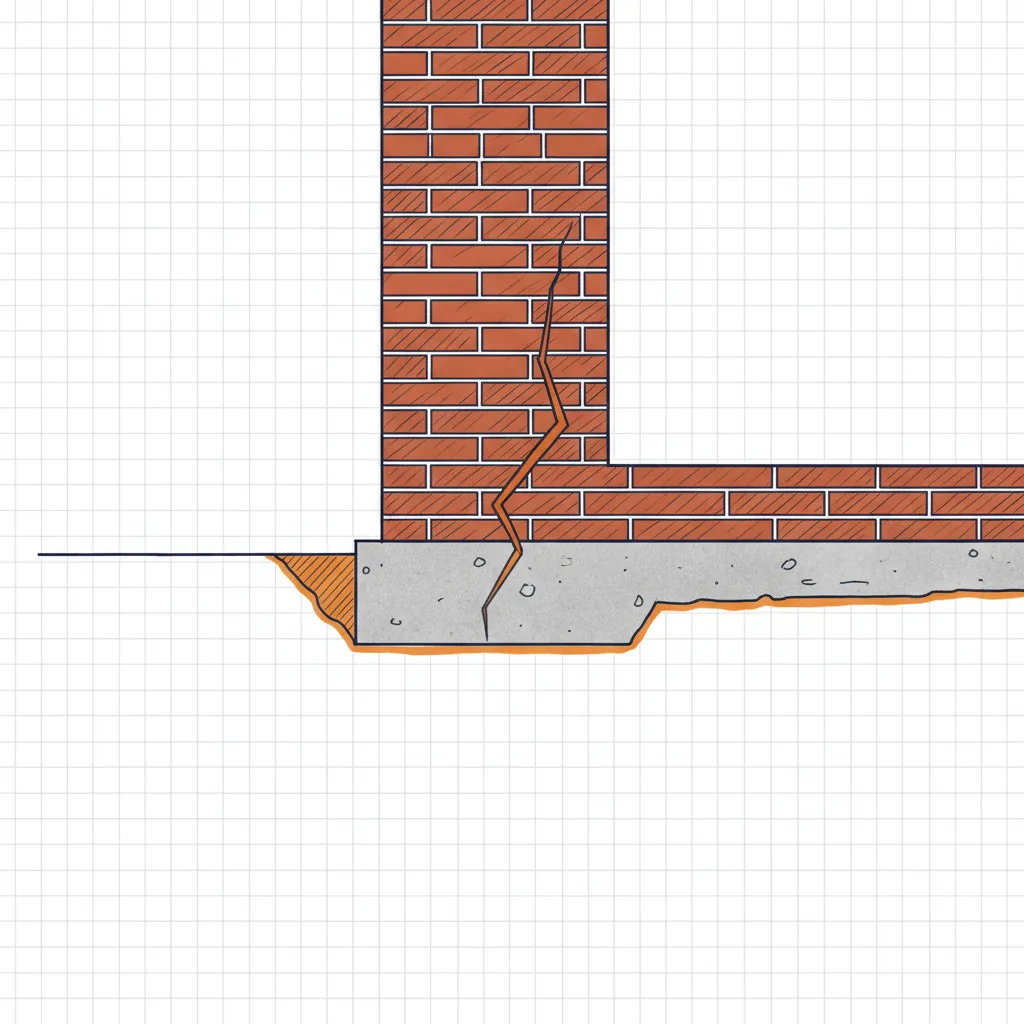

The Hidden Threat: Accidental Discharge of Water

The most common covered cause of foundation damage is an accidental discharge of water from a plumbing system. This is not a slow leak from a faucet; it is a sudden failure of under-slab pipes. A slab leak, a rupture in the plumbing beneath your foundation, can release thousands of gallons of water. This water saturates the soil, causing it to heave or erode rapidly, so you can experience a sudden and dramatic shift in your foundation. Because the plumbing failure is a sudden, accidental event, the resulting foundation damage may be covered, even though earth movement itself is excluded. The key is proving the plumbing failure was the direct and initiating cause.

Sudden & Accidental Events: Fire, Explosions, and Other Named Perils

Other named perils can also lead to a covered foundation claim. A significant house fire can compromise the structural integrity of the concrete and steel within the foundation. An explosion from a gas leak could crack the slab and footings. A large, falling tree could cause a localized collapse. In each scenario, the damage is a direct consequence of a sudden, identifiable event. The insurer is not covering the foundation in isolation; it is covering the holistic damage caused by a peril listed in the policy.

The Architect’s Proof: The Critical Role of the Engineering Report

An insurance claim for foundation damage is not a conversation; it is a presentation of evidence. The adjuster’s default position will be to cite the earth movement and settling exclusions. To overcome this, you must present irrefutable proof that a covered peril caused the damage. This proof is not a contractor’s estimate; it is a formal report from a licensed structural engineer.

Diagnosing the Cause: Why an Engineer’s Assessment is Non-Negotiable

A structural engineer’s report, a detailed diagnostic document, serves as the cornerstone of your claim. The engineer acts as an impartial expert, using soil samples, elevation measurements, and forensic analysis to determine the precise cause of the failure. This report shifts the claim from your opinion to an expert’s professional conclusion. It provides the insurer with the data required to approve a claim that would otherwise face certain denial. The investment in an engineering report, typically $500 to $1,500, is the cost of moving your claim into a defensible position.

| Evidence Type | Strategic Purpose | Operational Value |

|---|---|---|

| Structural Engineer’s Report | Establishes the definitive cause of damage. | Overcomes the insurer’s default exclusion-based denial. |

| Plumbing Leak Test Report | Provides direct evidence of a hidden water discharge. | Links foundation movement to a covered peril. |

| Repair Estimates from Foundation Specialists | Quantifies the financial scope of the loss. | Sets the financial parameters for the claim settlement. |

| Dated Photographic Evidence | Creates a timeline of the damage progression. | Demonstrates the ‘sudden’ nature of the event. |

Building Your Case: Assembling the Evidence Your Insurer Requires

Your claim submission is a business case for financial recovery. It must be clear, concise, and conclusive. First, commission the engineering report. Second, obtain a plumbing test report to confirm a leak if that is the suspected cause. Third, gather detailed repair estimates from reputable foundation companies. Finally, compile a photographic timeline showing the damage as it appeared and progressed. You submit this complete package with your claim, so the adjuster has all the necessary documentation to justify a payment from the outset.

Beyond the Standard Blueprint: Policy Endorsements and Specialized Coverage

The standard homeowners policy is a foundation, but it is not the complete fortress. Strategic asset protection requires fortifying this base with specific endorsements, which are policy add-ons that buy back coverage for certain excluded events. This is how you customize a generic policy to fit the specific risks threatening your assets.

Slab and Foundation Endorsements: Fortifying Your Texas Policy

The Foundation and Slab Endorsement, a crucial policy rider available in states like Texas, directly addresses the water leak exclusion. While a standard policy may cover the water damage itself, it often excludes the cost to tear out and replace the slab to access the broken pipe. This endorsement adds coverage for that specific expense, so you are not faced with a $10,000 to $15,000 bill just to begin repairs. Some endorsements go further, adding a limited amount of coverage (e.g., $15,000) for foundation damage resulting from a hidden water leak, closing a dangerous gap in the standard blueprint.

Earthquake and Flood Policies: Securing Against Catastrophic Ground Shifts

Catastrophic ground movement requires a dedicated defense. Earthquake Insurance, a separate policy, protects against damage from seismic activity. Flood Insurance, also a separate policy typically backed by the National Flood Insurance Program (NFIP), covers damage from rising surface water. Neither of these perils is covered by a standard homeowners policy. Integrating these policies into your plan is essential for achieving cohesive protection against large-scale geological events.

Constructing Your Financial Fortress: A Cohesive Risk Strategy

Protecting your home’s foundation is not an isolated task. It is a core component of a comprehensive asset protection strategy. Relying on a standardized, off-the-shelf policy is like building a castle with a dry moat, it provides the illusion of security while leaving your wealth vulnerable to predictable threats. A robust defense requires a cohesive, integrated plan.

Escaping the ‘Paper Legacy’ of Standardized Policies

Commodity insurance sold on price alone creates a ‘paper legacy’, a stack of policies that look complete but are riddled with structural gaps. Most homeowners are underinsured because they have coverage but no cohesion. Their policies are a collection of disconnected parts, not a unified defense. This fragmented approach leaves critical assets, like a home’s foundation, exposed to financial loss from misunderstood exclusions. Proactive planning replaces this vulnerability with strategic certainty.

Integrating Your Home’s Foundation into a Unified Asset Protection Plan

Your home is not just a dwelling; it is a significant financial asset that anchors your balance sheet. Its protection must be integrated into your total financial blueprint. We analyze your home’s unique risks, from soil type to construction age, and architect a policy structure that closes the gaps left by standard contracts. We then align this structure with your liability coverage, your auto policies, and your estate plan. This method transforms disparate policies into a unified financial fortress, so you can ensure your life’s work is built on a foundation of strategic certainty.